I recently prompted a conversation about smart building technology deployment strategies that at times appeared to prompt a “Oh No It Isn’t – Oh Yes It Is” pantomime like back and forth, or at least on LinkedIn. That totally missed the point of my original post (see here and here) and ended up with me playing both agony aunt and punchbag to different stakeholders involved during facilitating the exchange (I hope among playing other more productive roles). This one is really a reflection on one way I go about looking at what is going on in the smart buildings technology space with this business model environment lens from the folks at lean startup specialists Strategyzer (see more in it here). As well as what I am seeing by using it, and how that has all the makings of an interesting panel discussion.

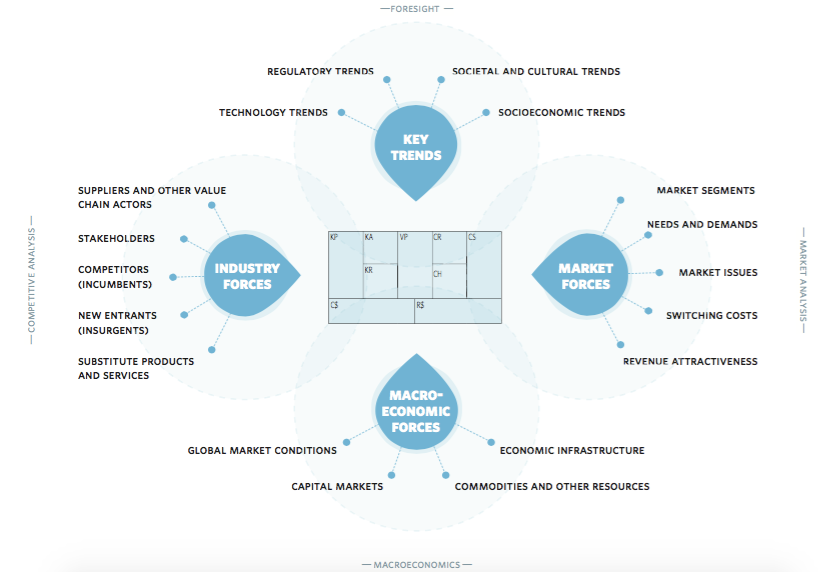

The business model environment lens is a combination of Porter’s Five Forces Analysis Model, PESTEL Analysis and probably longer list of lenses you can find over on Gennaro Cuofano‘s 4 Week MBA resource that I have mentioned previously (see more here). And one that looks at industry forces and key technology trends (among other things).

It’s just that I have seen a number of announcements about partnerships/alliances between major Operational and Information Technology players. That includes ‘ABB partnering with with Samsung Electronics to drive holistic smart building technology,’ a ‘co-innovation partnership with Cisco and Schneider Electric,’ among other news about acquisitions e.g., Samsung acquiring Harmen who own AMX (see here) or Mitsubishi Electric ‘fully acquiring’ Iconics (see here). There’s probably more that hasn’t crossed my radar and/or on the horizon.

Arguably there’s nothing new here given likes of the Avanade collaboration between Accenture and Microsoft, and their broader alliance. And that being interesting because of Microsoft Azure ‘accelerating smart building solutions with investments in cloud, AI, and IoT‘ and Accenture’s expertise in workplace system integration very likely extending into smart building systems integration as PropTech and WorkTech worlds continue to blur.

That blurring of lines was evident at recent WorkTech London event I attended where sessions on both smart buildings and smarter workplaces sat side by side. And seems baked into the Smart Building Conference in Barcelona by being one of the conference strands at ISE (Integrated Systems Europe), ‘the worlds leading AV and systems integration show.’

Google’s Building Operating System is another example of what I am on about here being a thing and for some time, along with how those with careers in AEC Industries and also Building Operations are being recruited by IT players both hard and soft, as well as consultancies.

I mention Google because some I speak to think it would be a mistake to see all this partnering/alliancing being a move by the big operational tech players into IT but arguably the other way round and with soft rather than hardware side of that potentially representing the bigger threat. In the meantime, it will be interesting to see who will end up eating whose lunch.

What’s nor clear, particularly with the Big IT/OT partnership announcements, is if and how these help drive innovation or whether they are actually more sales and marketing-led. And on that note, there is probably an interesting discussion to be had about whether they are boon or barrier for technology innovation in smart buildings. Certainly, those I speak to at the sharp end of integration and smart building enablement think the real innovation is coming from a new breed of those analysing and automating data who can be more nimble and agile than the bigger players.

At the same time, those MEPs and (Master) Systems Integrators also see innovation occurring with technologies that are helping bring about the Independent Data Layer that probably needs a separate post. You could probably include all those technologies, IoT and otherwise, from smaller players you find in the growing number of market places including those from major players or those they own, e.g. Tridium’s Niagra Marketplace.

Personally, it would be more interesting to extend that discussion to ask whether innovation in general is happening more or not in retrofit i.e., rather than in new/rebuilds or larger-scale refurbishments that also start with blank piece of paper having stripped everything back to shell and core.

Now that would be a panel session I would like to attend and ideally curate/moderate, so if anyone wants a thought provoking session for their event and/or as part of their marcoms activities then please get in touch.